By Dimeji Macaulay,

Preamble

As a tax justice campaigner, I feel compelled to put a clarion call on youth, workers’ movements, civil societies, community members and trade union leaders, to mobilize and advocate against anomalies in tax treaties and tax holidays which only benefit multinational corporations in Nigeria and parts of Africa; and by so doing, we all rise up to collectively fight to end revenue linkages.

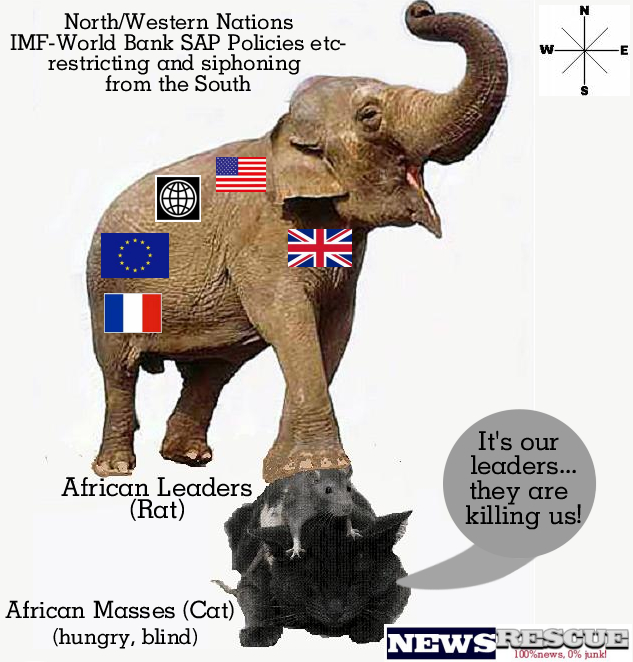

One of the leading African political writers, Walter Rodney, in his book: “How Europe Under-developed Africa”, examined how our continent have been shortchanged and placed on permanent starvation for decades of colonization and after decolonization by the imperialist world powers.

With this backdrop, I arose from the training sessions held by both ActionAid Nigeria and African Submit on Tax Treaties between February 22nd and 23rd cum 24th and 25th, separately and in different settings, focusing on tax treaties, with a curiosity that fueled my angst.

Tax treaty and those involved

Without doubt, many an average reader would be conversant with the concept of Tax Treaties. But for the benefit of those who are not, tax treaties are agreements signed between governments of countries and often times with administrators of multinational companies to permit them come into a country and invest without paying tax. It also affords opportunities to indigenes of the country to go and establish in a representative country without paying tax. Given this, tax treaties can be referred to as Double Tax Agreements (DTAs), Double Tax Treaties (DTTs) or Double Taxation Conventions (DTC).

Unfortunately, however, the process and conducts African leaders deploy in contracting the treaties without due recourse to economic experts’ inputs have dealt what could have earned their respective countries huge economic gains, a huge blow. As such, whatever profits the treaties may score for respective countries are largely compromised.

For the benefit of convictions, tax treaties decide how much the contracting states can levy multinational companies and other cross-border activities. In the instance of Nigeria, a research reveals that we lose about five hundred billion in naira, an approximate of ($3.3billion), to tax treaties in the last five years because many of the multinational companies in the country denied their workers living wages. Consequently, the research says, many employees are placed on poverty wages despite being the wealth creators and operators of their respective multinationals sweatshops.

However, there is a good side to tax treaties which can only be utilized had respective governments, while adopting the agreements, insert a notification to local investors to also go to the same countries they signed treaties with, to set up businesses so that they can equally enjoy tax treaties. But by Nigeria and African standards, it is quite doubtful if our local investors or business owners have the financial muscles to enter other countries to institute industries.

To this extent, our governments have operated and endorsed tax treaties in ways that are beneficiary only to mostly foreign multinationals and respective regime’s agencies as the main actors excluded especially domestic business owners and other extended beneficiaries.

What they fail to admit and acknowledge is that many of the bilateral tax treaties govern what taxing rights developing countries have, but frequently reduce the rights of poorer countries to tax theses flows.

{kind=link}